Boy Wirat

There’s a problem brewing right now that I suspect too many investors are unaware of, even though it’s happening right in front of their eyes. And it’s a problem that, if it continues a bit longer and a bit further than it already has, threatens a lot of wealth that people did not expect to be “in play.” Because while it seems so many eyes are focused on the headline stock market indexes or finding high dividend stocks, there’s one thing that has the potential to blow all of that well-meant effort out of the water. And while I’ve written about it many times here, I’m now going to try to do so in a way that does three things:

1. Identifies the problem, clear as day, to any investor.

2. Introduces a way for investors to stay alert to determine if the problem is about to go from bad (now) to worse (later).

3. How to either hedge or exploit this budding market issue, and potentially be one of the relatively small number of investors that not only doesn’t get crushed, but potentially even makes money in the event things get worse.

OK, enough drama to set the scene, now to the specifics. Because truly, as someone who has watched the markets closely since the 1980s, this is some time to be an investor!

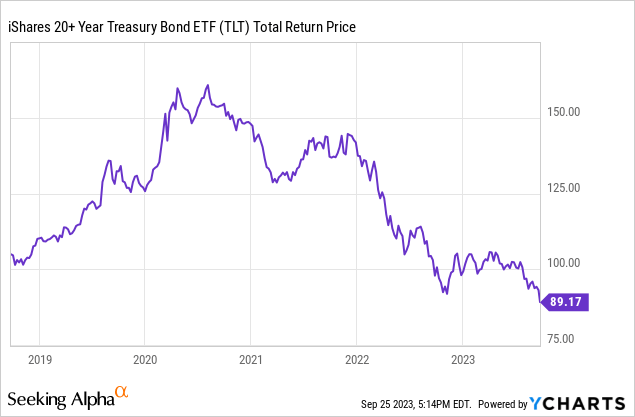

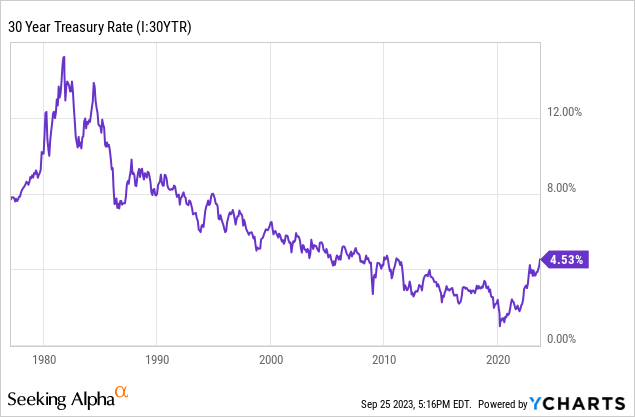

I’m showing these charts of TLT and the 30-year US Treasury bond yield because the analysis below all starts here. Specifically, with a breakdown in TLT’s price below a key level, and the long-term breakout in yield that ends a downtrend in place for about the past 35 years. Yes, 35 years, back to 1988. That’s serious.

Markets are showing cracks around the edges. But nearly all of the edges. And based on a lot of the commentary on Seeking Alpha and elsewhere, there’s a growing feeling that “something” is about to break. But what that something is, doesn’t really matter until it happens. If it happens at all. And if something comes along to “break” the markets, the only thing that will matter is how an investor is positioned for it when it breaks, and how to seize on the opportunity to exploit the break, while most investors scurry about, making panic moves and guessing.

We’ve also had many false alarms for the past decade or so, and the Fed has come to the rescue each time to make it all better. The stock market has had an amazing long-term run, enough to convince a new generation of investors that this is the way it always work.

Spoiler alert: The markets don’t always work like they did in the past 10 years

During the past 10 years, stocks have mostly gone up, and they did so in large part because the bond market was enabling that. Interest rates and inflation were near zero, government debt was not insurmountable, and consumers didn’t sweat carrying lots of credit because the rate to pay it off was so low. That is no longer the case.

What’s happening now is not anything that hasn’t been happening for several months now. The difference, as I’ve written about and spoken about recently on Seeking Alpha’s Investing Experts Podcast, is that the markets are starting to care about the debt, the lagging impacts of those 11 rate hikes, China’s growing problems and more. And again, what matters in the markets is not what we all read and wax poetic about concerning the markets.

It’s the price action that matters. And when it comes to what’s likely to drive the stock market the rest of the year and into next year, price is starting to speak very loudly. The price I’m talking about is that of long-term US Treasury Bonds, represented below by ETF ticker TLT.

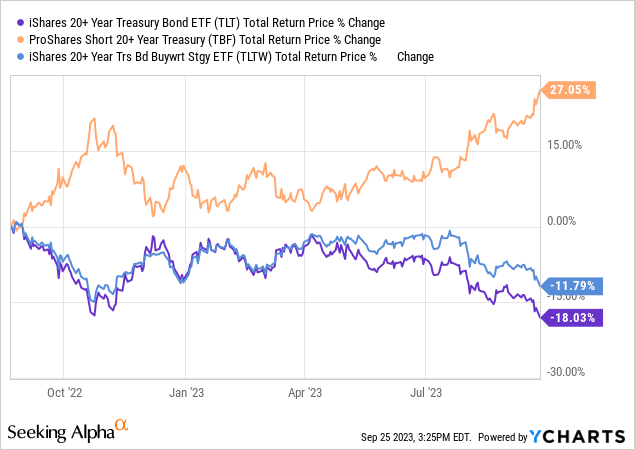

You also will see two other ETFs that in the covered call ETF universe I follow and have been writing about, are “cousins” of TLT. One is TLTW, a covered call writing ETF that owns TLT, but writes calls against that entire position, rolling those calls monthly. I own TLTW personally. In fact, it’s my largest single covered call ETF position, larger than each of the equity and commodity covered call ETFs I own.

But TLTW, as much as I like it, needs help in a market like this. And that’s why the focus of this article is on ProShares Short 20+ Year Treasury ETF (NYSEARCA:TBF), which might be the most opportunistic ETF I’ll own the rest of this year. That’s because TBF is structured to go up when long-term US Treasury bond prices go down. That’s the same thing as when long-term US Treasury rates go up. And they’re going up.

Furthermore, they’re showing strong signs that their recent pop higher is the beginning of a move, not the end. It’s a 14-year-old ETF with a mere $192 million in assets in it. That it doesn’t have many times that amount signifies to me that “everyone” is watching the stock market, while the bond market is not only the “tell” for the stock market these days, it’s also an opportunity to potentially make a lot of money in a difficult investing environment.

Note that as with all inverse ETFs, anyone considering an investment in it should really do their homework. There is a slight leverage factor here (25%) and TBF is designed to perform opposite TLT on a daily basis. The longer you hold it, the more likely its performance will diverge, even slightly, from the opposite of TLT.

3 portfolio implications:

1. If the bond market stabilizes, TLTW is a great ETF to hold, and I will continue to hold it.

2. However, if rates continue to bust this move higher, TLTW provides me with a nice level of income, but its price risk is high. Just look at the chart above, showing TLTW since its 2022 inception. It’s down nearly 12% since it debuted. What a terrible ETF, right? Wrong. TLTW is spinning out a yield of over 13%, and unlike a dividend equity ETF or a high-yield bond ETF, we know exactly what drives it: The interest rate on 20-30 year US Treasury bonds! Easy enough to track, and as a long-time chartist, I let the charts guide me, not the noise.

3. And, if rates rise even more, I’m holding my TLTW, but bringing in some help. While I do own some TLT put options and trade them on a short-term basis to try to turn small amounts of capital into large ones as TLT’s price has broken down (and continues to), that’s a more nuanced strategy. So I explain it more on the surface here, since option trading knowledge is not easily transferable, especially in short articles like these.

The easier strategy to transfer my knowledge on in this space is as follows: TLTW is a long-term holding, at least I aim for it to be for me. But TBF is a tactical holding that I own in sync with TLTW, because owning it keeps the dividends from TLTW flowing, but cuts down on the impact on my portfolio of those rising rates. So at a time like this, having some TBF paired with my TLTW allows me to get the income but cut some of the price decline. The more TBF I own as a percentage of my TLTW position, the more protection I get. And, if I decide to really “go for it” during this bond rate cycle, I could end up owning more TBF than TLTW, essentially creating a “net short” position in the bonds, but still getting that cash flow from TLTW.

The technical picture

And with a recent breakout after a brief but tough battle around long-term “support,” TLT has broken down again. And this time, the projected downside is, well, not something we can gauge based on anything that’s happened since TBF launched in 2009. So I smell opportunity.

Yet if this turns out to be a total fake out, and the long bond yield’s move to new high territory is short lived, there’s another ace in the hole, so to speak. Because one scenario many are hoping for is that the Fed starts to signal that it will cut rates. And though they only control overnight lending rates, history indicates that could cause long-term US Treasury rates to fall sharply as well, as a “flight to quality” trade kicks in. Because a rate cut at this point would be a strong signal that something is very, very wrong in the economy.

So, if any of that happens, or more properly “when” it happens – because rates will go down again someday – there’s the other member of this threesome: TLT. By swapping out the TBF position for some TLT, and continuing to hold TLT, I get the other thing TLTW can’t do on its own: Make a lot of return beyond the coupon when rates fall. That’s because TLT rises in price, but quickly runs into a wall in the form of the covered call option strike price in TLTW, which is set just a little way above the current price. But the problem is solved for those who want to try to piggyback an eventual decline in rates, by having TLT warming up in the bullpen, so to speak.

Rob’s covered call ETF strategy: Summarized

That’s the beauty (to me) of how this entire concept of using covered call ETFs at the core of my portfolio, but managing around it with other ETFs and options is a central part of my retirement portfolio. The rest of it is simply in T-bills and T-bill ETFs for now.

The history: It’s been a while

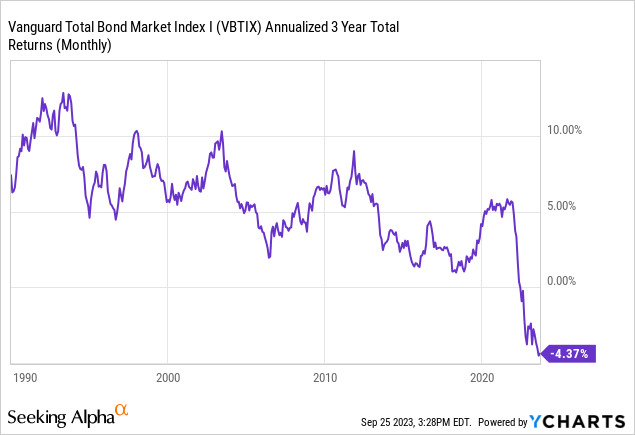

There’s no ETF that can truly capture the level of decline in prices and increase in interest rates that is potentially at hand in the coming 6-12 months. We have not had a period like this since ETFs were first created in 1993.

I had to go back and find a bond fund of some sort that went back further. I still only got as far back as 1990, and this Vanguard Bond fund. But you can see on the far right why this is dangerous territory for those who don’t make themselves aware of innovative and modern tools like TBF, and TLTW as well.

We are looking above at a three-year rolling return on a generic bond portfolio of -4.4% a year. That will, at some point, become more than an issue financial advisors and investors can ignore. I think that time of reckoning is approaching rapidly. And I’m basing it on a strong, though never perfect, signal from the chart of TLT, which is breaking down faster and faster as the weeks continue.

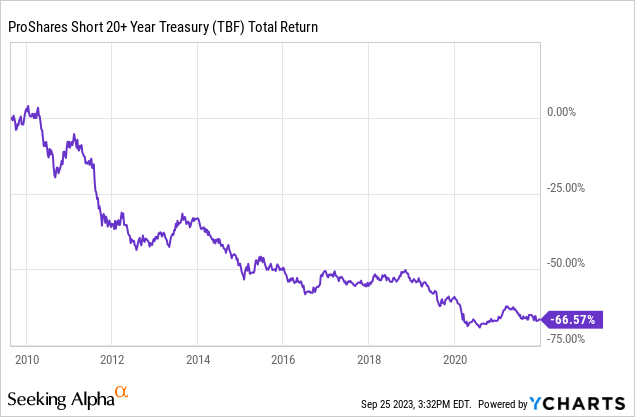

Finally, here’s one more chart to show why this is not selective memory about the risks and opportunities of rising rates. There’s no memory at all! Because TBF, the anti-bond bull ETF, has done nothing but go down for most of its 14-year life. Of course, that’s the case! Bond rates have been falling since the early 1980s, with little reprieve.

But finally, here in the autumn of 2023, there is a possibility that shorting long bonds in this way, while still getting the income from sources like TLTW (for me, at least), is emerging as a potentially straighter path than trying to find stocks or bond ETFs that have unexpected credit or other risks. And given all of the great comments and Q&A I’ve had with so many in the Seeking Alpha comments section of my articles lately, I plan to continue rolling out more advanced discussions on how I use covered call ETFs, and how I navigate around them with additional, tactical ETF positions to pursue retirement income... without the high risk of massive principal loss I see in many other income strategies.