Pinterest (NASDAQ:PINS) recently reported its Q3 results, sparking renewed market interest with strong numbers. As the go-to platform for ideas, spanning from home remodeling to tattoo designs, Pinterest stock saw a notable surge driven by substantial user growth, heightened revenues, and improved profit margins. Despite these positive signals, my caution prevails. I suspect that analysts are likely overestimating Pinterest’s earnings potential. In fact, shares look overvalued. Thus, I’m bearish on the stock.

User Growth Was Commendable

Pinterest’s post-earnings surge was driven by the company posting commendable user growth. In a landscape where users’ attention is scattered across diverse social media platforms, Pinterest has managed to maintain a stronghold by continuously engaging an ever-expanding user base on its unique idea-sharing platform.

As the quarter concluded, Pinterest celebrated a significant milestone with a record-breaking 482 million monthly active users (MAUs), marking a notable 8% increase year-over-year. This achievement not only signifies the platform’s resilience but also surpasses its peak user count observed during the pandemic surge. This growth is attributed to Pinterest’s strategic shift towards enhancing its unique qualities as a platform for visual search and discovery and its evolution into a shopping destination.

What sets Pinterest apart is its ability to facilitate dynamic multi-session journeys, allowing users to seamlessly transition from inspiration to action. The post-earnings conference call shed light on the robust user engagement facilitated by this approach. Users can effortlessly save and curate ideas and products, whether for immediate use or future reference, creating a continuous exploration experience with each visit.

Central to this success is the platform’s algorithm, which consistently refines its recommendations to enhance relevance. This, in turn, crafts user journeys across various verticals, leading to actionable outcomes such as refreshing wardrobes, discovering gift ideas, or planning travel itineraries.

Additionally, the platform’s knack for creating content that effortlessly fits into a marketplace setting aids in revenue generation for both brands and creators. This synergy between user engagement and revenue generation highlights the effectiveness of Pinterest’s model, making it not just a social media platform but a dynamic space where inspiration transforms into tangible outcomes.

But User Growth Doesn’t Solve Pinterest’s Main Problem

Certainly, Pinterest’s commendable user growth and growing engagement in the current market climate are noteworthy. Yet, they don’t alleviate the company’s primary challenge — an inability to generate meaningful profits. Let’s break down the situation step by step. Despite Pinterest’s revenue growth of 11% to $763 million in Q3, it’s essential to note that this increase was primarily driven by a larger user base rather than a substantial rise in the average revenue per user (ARPU).

The crux of the issue lies in the fact that user growth occurred predominantly in regions with limited monetization prospects. Specifically, while monthly active users (MAUs) increased by a substantial 12% in the “Rest of World” markets, which comprise emerging markets, this metric only saw marginal growth of 1% and 7% in the U.S. & Canada and Europe, respectively. Unfortunately, emerging markets pose challenges in terms of monetization.

The real revenue potential lies in the U.S. & Canada, where advertisers are more willing to spend on ads. To put this into perspective, the company’s ARPU for Q3 reached $6.46 in the U.S. and Canada, in stark contrast to a modest $0.91 in Europe and a meager $0.12 in the Rest of World segment. Essentially, a user from the U.S. or Canada is valued as much as 53 users from an emerging market country.

This is quite problematic, as despite the noteworthy user growth contributing to some revenue increase, Pinterest seems to have hit a plateau in regions where it can generate substantial revenue. This is evident from the mere 1% user growth in the U.S. and Canada, even during what seems to be a robust quarter in terms of user engagement.

Consequently, Pinterest continues to grapple with the same challenge it has grappled with for years— the inability to generate significant profits. Sure, user growth did drive higher revenues, which, in turn, resulted in an improvement in operating margins. Specifically, operating losses narrowed from the previous year’s $69.4 million to about $5.0 million. However, the company continues to operate at a loss.

Notably, the reported net income of $6.7 million was primarily attributed to generating $26.7 million in net interest income from its cash position, resulting from rising interest rates rather than sustainable business operations. This underscores the persistent struggle Pinterest faces in finding a long-term solution to its profitability dilemma.

Even if Pinterest manages to break even with its expanding scale, there seems to be no evident path for the company to attain an operating profit in the hundreds of millions. Therefore, the stock’s current valuation, with a market cap of $21.2 billion, suggests a gap between expectations and true profitability potential.

Is PINS Stock a Buy, According to Analysts?

Regarding Wall Street’s sentiment on Pinterest, the stock features a Moderate Buy consensus rating based on 19 Buys and nine Holds assigned in the past three months. At $35.30, the average Pinterest stock price target implies 12.1% upside potential.

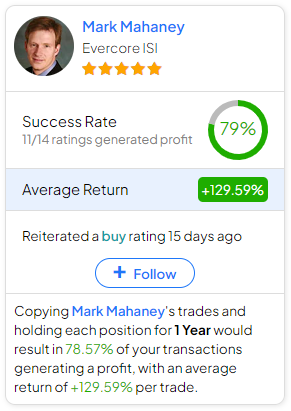

If you’re wondering which analyst you should follow if you want to buy and sell PINS stock, the most profitable analyst covering the stock (on a one-year timeframe) is Mark Mahaney from Evercore ISI, with an average return of 129.59% per rating and a 79% success rate. Click on the image below to learn more.

Conclusion

In conclusion, while Pinterest’s robust user growth is undeniably commendable, it doesn’t resolve the core issue at hand—the company’s ongoing struggle to translate its expanding user base into meaningful profits. The Q3 revenue surge, driven primarily by increased users, masks the challenge of effectively monetizing emerging markets. Despite improvements in operating margins, Pinterest’s profitability remains elusive.

In the meantime, the stock’s post-earnings rally has pushed the stock’s valuation to unjustifiable levels. Shares are currently trading at a forward P/E of about 30 based on Wall Street’s FY2023 EPS estimates, a multiple that I find totally absurd given that Pinterest is effectively operating at a loss. For context, Meta Platforms (NASDAQ:META), which is printing cash, has more apparent growth prospects, and features a higher margin of safety, trades at a forward P/E of just 23.

As such, my caution persists, and I maintain a bearish outlook on Pinterest’s stock.

Disclosure

Source link

credite